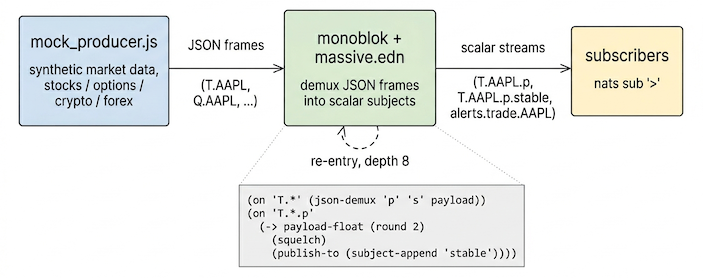

Market data moves fast. Imagine your data provider gives you a stream of JSON frames that carry several fields per message, and every downstream subscriber re-implements the same demux, round, dedupe, alert logic. At scale, doing this n times causes read/write amplification and much wasted work, not to mention subtle bugs. Doing it once at the broker means that subscribers can use subject filtering to pick the slice they actually need and ignore the rest.

Three monoblok rules can get you there.

Each frame carries several fields, so rule 1 splits them out into one subject per field (a demux). Rule 2 cleans the price stream. Rule 3 watches for jumps. Each rule feeds the next.

;; 1. Demux the JSON frame into per-field scalar subjects.

;; T.AAPL { "p": 187.42, "s": 100 } becomes T.AAPL.p, T.AAPL.s

(on "T.*"

(json-demux "p" "s" payload))

;; 2. Round to 2dp, drop duplicates, mirror to .stable.

(on "T.*.p"

(-> payload-float

(round 2)

(squelch)

(publish-to (subject-append "stable"))))

;; 3. Alert on a >= $1.00 jump between consecutive ticks on the same symbol.

(on "T.*.p"

(when (>= (abs (delta payload-float)) 1.0)

(publish

(str-concat "alerts.trade." (subject-token 1))

payload)))

That is the entire conditioning layer for stock trades. Options come along free (the T.* wildcard matches T.O:AAPL250620C00200000 too), crypto and FX repeat the pattern with their own thresholds. Full file: massive.edn.

A subscriber that only cares about price changes subscribes to T.*.p.stable and gets a clean, per-symbol stream of rounded floats. No JSON parsing, and no need for every consumer to chew through the firehose and repeat the same logic.

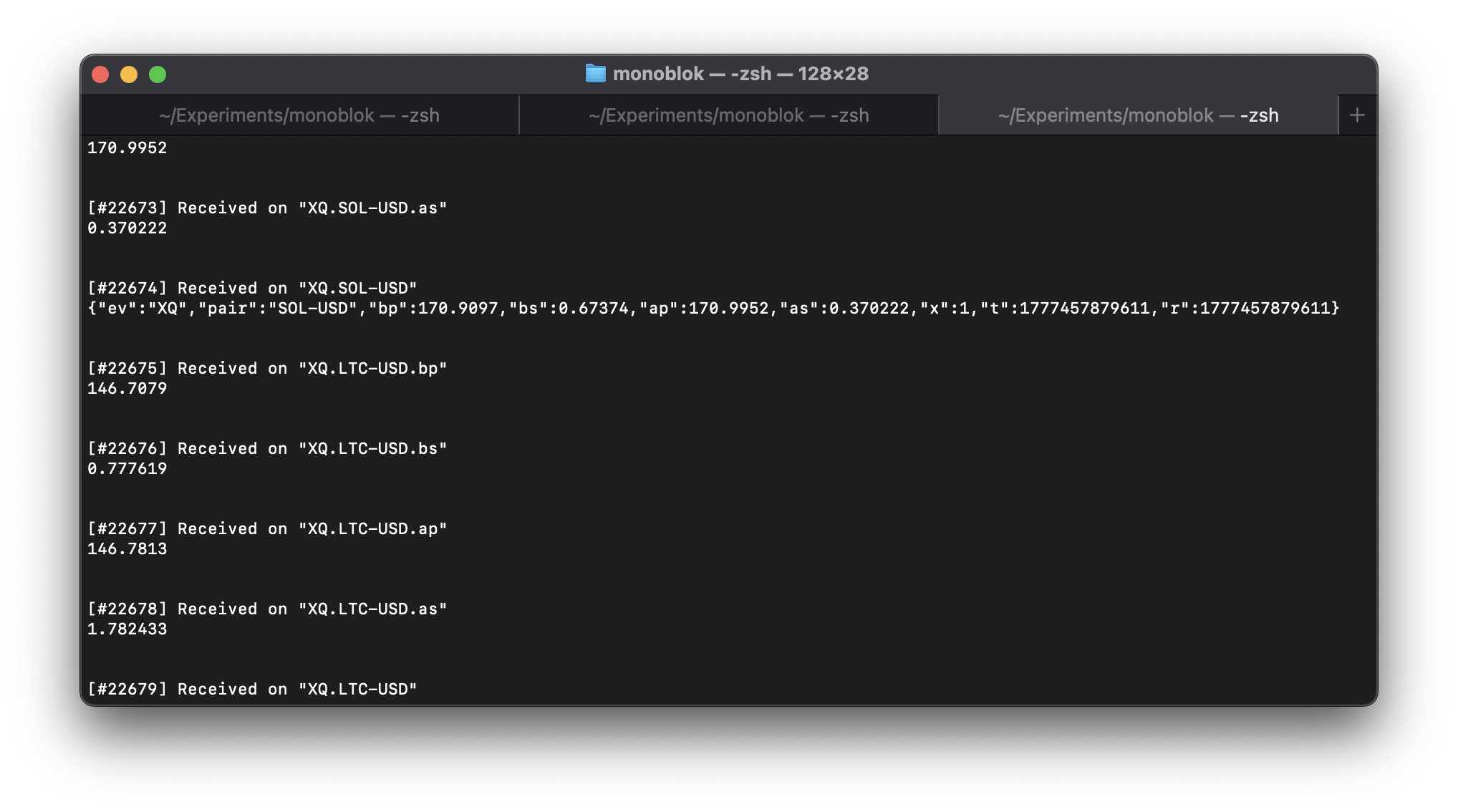

A working example sits in the monoblok repo at examples/json-massive. It simulates the Massive websocket market data feed (stocks, options, crypto, forex) being conditioned by patchbay rules at the broker. The producer is a Node script that speaks the NATS protocol over a plain socket and publishes synthetic frames on subjects shaped <ev>.<symbol>. Open three terminals and run:

# 1: monoblok with the demuxing patchbay

monoblok --port 4222 examples/json-massive/massive.edn

# 2: the synthetic producer

node examples/json-massive/mock_producer.js

# 3: peek at everything

nats sub '>'

A glimpse of it running on the crypto quote channel (XQ.*), where the raw frame and the per-field scalars land side by side. The trade flow on T.* is the same shape: raw frames alongside demuxed T.<sym>.p and T.<sym>.s scalars, plus a deduplicated T.<sym>.p.stable mirror and any alerts.trade.<sym> triggers.

If you’re new to monoblok, the introductory post covers the primitives. Rules 2 and 3 above also depend on a feature that didn’t exist a week ago: as of 0.0.28, publishes from patchbay rules can re-enter the rule engine, which is what lets these three rules feed into each other.

Re-entry, capped at 8

The interesting bit is rule 2 matching T.*.p, a subject that only exists because rule 1 emitted it. In 0.0.28, a publish produced by patchbay itself is now eligible to match downstream rules. Previously it would have been forwarded to subscribers and that was that, so a staged pipeline like the one above had to be flattened by hand into one rule that did everything inline. Awkward, especially when several rules want to feed off the same demuxed scalar.

Re-entry is the obvious thing to want and the obvious thing to be nervous about. A rule that emits a subject which matches itself is a feedback loop: howl, except in subject-space. The cap is 8: a publish can re-enter the rule engine up to 8 times in a single causal chain, then it stops. Long enough for any reasonable staged pipeline (demux, condition, mirror, alert is 3 or 4), short enough that a misconfigured terminates, with a warning, almost immediately.

This release also lets : appear in subjects, which matters here because options use OCC symbols like O:AAPL250620C00200000. The single (on "T.*" ...) rule covers stock and options trades because the wildcard happily matches the colon-bearing token.

Free LVC for slow markets and the close

A dashboard opening on Sunday afternoon wants to render the last print for every symbol it tracks. Nothing is publishing, the market is closed, and the patchbay has been idle for two days. Subscribe to $LVC.T.*.p.stable and the broker hands back the most recent rounded price for every symbol it has ever seen, then nothing else until trading resumes. Same one-shot subscribe works for a logger restarting mid-session, or a tool that just wants the last print on a thinly-traded name where ticks arrive minutes apart.

The subject last-value cache (LVC) is a built-in feature of monoblok, on by default. It comes along for free with anything the patchbay publishes: the demuxed scalars on $LVC.T.*.p, the deduplicated mirror on $LVC.T.*.p.stable, and the raw frames on $LVC.T.*. No JetStream stream, no external KV, no extra rules. The dedupe rule above is what makes the .stable LVC actually useful too: without squelch, the cached value would be whatever noisy reprint happened to land last, rather than the last meaningful price.

Already-aggregated channels

A small aside that’s worth knowing if you’re poking at the real Massive feed rather than the mock: the AM / XA / CA channels deliver server-side OHLC bars when using a -delayed feed. The patchbay just demuxes those into scalar o / h / l / c / v streams instead of recomputing bars from raw trades. If you only have a trade stream and want to build bars yourself, there’s a bar primitive and a separate examples/bars.edn for it.

Bridging to NATS

Subscribers can hook up directly to monoblok and it works fine. Most of the time though, you already have a NATS cluster doing the heavy lifting for the rest of the system, and you want the conditioned market data to land there too. monoblok ships with a bridge that forwards selected subjects to a downstream NATS server, so the conditioned streams can flow into JetStream without the broker having to redo any of the work. Point it at T.*.p.stable and JetStream stores the deduplicated, rounded prices, not the raw firehose. Less write amplification, less retained noise, and only the precision a consumer actually needs.

This sharpens a few things downstream. Per-message dedupe windows in JetStream have less to chew on because squelch already collapsed redundant messages upstream. Replays are smaller and faster. Consumers reading from the stream get the same shape of data as live subscribers on the broker, which means a backfill and a live tail stitch together cleanly. The raw frames stay on the monoblok side for anyone who wants them, but nothing forces JetStream to pay the storage cost.

Try it

git clone https://github.com/lexvicacom/monoblok

cd monoblok

./examples/json-massive/run.sh

This will run monoblok, the synthetic producer for 5 seconds, and prints tables of the raw frames, the demuxed prices, the stable mirror, and the alerts side by side.

Binaries are on the releases page if you would rather not build from source. The earlier playground post is the easiest way to get a feel for the primitives without running anything locally.